How to Handle VAT on Amazon When Selling in Multiple EU Countries? A Complete Guide

Spis treści

At first, it doesn’t look like a big deal. You register your business, maybe get a VAT number in your home country, and start selling. But the moment your orders start crossing borders—or your stock ends up in more than one warehouse—things get complicated fast. Rules start stacking on top of each other, and what felt like a simple expansion suddenly turns into a maze of registrations, thresholds, and reporting obligations.

The core issue is this: selling on Amazon in the EU isn’t just about selling more—it’s about operating across multiple tax systems at the same time. And those systems don’t always play nicely together.

Multiple countries, multiple rules

Every EU country has its own tax authority, its own processes, and its own expectations. Even though there’s a shared framework for VAT across the EU, the practical side of things still happens at the local level. That means if your business touches multiple countries, you’re potentially dealing with multiple sets of rules.

This becomes especially real the moment your stock moves. If your products are physically stored in a country—even if it’s Amazon moving them for you—that country may expect you to register for VAT there. It doesn’t matter if you haven’t made a single sale yet in that market. The presence of stock alone can trigger obligations.

And then there’s the customer side. Selling to consumers in different countries can mean applying different VAT rates depending on where the buyer is located. Suddenly, your pricing, margins, and reporting all depend on geography in a way that isn’t always obvious at first glance.

Amazon logistics don’t follow simple tax logic

Amazon is built for speed and efficiency. Its fulfilment network is designed to move your products as close to the customer as possible, often without you even noticing where your stock ends up. From a logistics perspective, it’s brilliant.

From a VAT perspective, it can be a headache.

You might send your inventory to one country, thinking you’re operating locally, only to find that Amazon has redistributed your stock across several countries to optimise delivery times. Each of those movements can create new tax obligations. In some cases, you’re expected to report these stock transfers as if you sold the goods to yourself across borders.

That’s the disconnect. Amazon simplifies selling, but VAT doesn’t simplify just because Amazon is involved. The system still expects you to track where your goods are, where they’re going, and who you’re selling to—and to report all of that correctly.

What this guide will help you do

This guide is here to cut through that complexity. No legal jargon, no abstract theory—just a clear, practical breakdown of how VAT actually works when you’re selling on Amazon across multiple EU countries.

You’ll see how different fulfilment setups affect your obligations, when you really need to register for VAT in another country, and how tools like OSS fit into the bigger picture. More importantly, you’ll see real scenarios that mirror how sellers actually operate, so you can connect the dots to your own business.

The goal isn’t to overwhelm you with rules. It’s to help you understand the structure behind them, so you can make smarter decisions as you grow.

Who this guide is for

If you’re a young e-commerce founder based in the EU, already selling on Amazon or planning to expand beyond your home market, this is for you. Maybe you’ve started seeing orders from other countries and you’re wondering if you’ve crossed some invisible VAT line. Or maybe you’re considering switching to FBA in more countries but aren’t sure what that means tax-wise.

This is also for non-EU sellers looking to enter the European market through Amazon. The opportunities are huge, but the VAT landscape is different from what you might be used to. Understanding it early can save you a lot of time, money, and stress down the line.

Wherever you’re starting from, the aim here is simple: help you move from confusion to clarity, and from guesswork to a setup that actually works.

The Foundations: How VAT Works for Amazon Sellers in the EU

Before getting lost in registrations, thresholds, and Amazon settings, it helps to zoom out for a second. VAT in the EU isn’t random. It follows a structure. And once you understand that structure, most of the confusion starts to fall away.

At its core, VAT for Amazon sellers revolves around two simple questions. Where are your goods physically located, and where are your customers based? Everything else builds on top of that.

The Two Factors That Control Everything

If you strip away all the complexity, VAT obligations for Amazon sellers in Europe are driven by two things that sound almost too obvious to matter. But they matter more than anything else.

The first is where your stock is stored.

This is the physical side of your business. Not where your company is registered, not where you live, but where your products actually sit before they’re sold. If your inventory is stored in another EU country, that often creates a local VAT registration obligation there, even if it does not necessarily mean you have a fixed establishment in that country.

For Amazon sellers, this situation usually comes up when stock is moved across borders into a fulfilment centre in another Member State. From a VAT perspective, that movement is often treated as a transfer of your own goods within the EU, which is why a registration may be required.

This is where many sellers get caught off guard. You might think you’re operating from one country, but once your inventory is physically present somewhere else, your VAT obligations can expand with it. It’s not about where your business feels based—it’s about where your goods actually are.

The second factor is where your customers are located.

This is the sales side of the equation. When you sell to consumers in other EU countries, VAT is generally due in the country where the customer receives the goods. That means the VAT rate applied to your sale may change depending on where your buyer is located.

This is what turns simple cross-border shipping into something more complex from a tax perspective. You’re not just reaching new customers—you’re stepping into different VAT jurisdictions with every order.

Put these two factors together, and you get the full picture. Stock location often determines where you need to register, while customer location determines how VAT is charged and reported on your sales.

The Golden Rules (Simplified)

Once you understand those two drivers, a few practical rules start to emerge. These aren’t edge cases or technical exceptions. They’re the patterns that apply to most Amazon sellers operating across the EU.

The first rule is simple, but important. If you store stock in another EU country, this will often trigger a local VAT registration obligation there. In practice, this applies to most Amazon FBA setups where inventory is held in multiple countries.

The second rule comes into play when you sell across borders to consumers. If you’re shipping goods from one EU country to customers in another, the One Stop Shop, or OSS, can simplify how you report VAT. Instead of registering in every country where your customers are based, you can report eligible cross-border B2C sales through a single EU country where you register for OSS, usually your country of establishment.

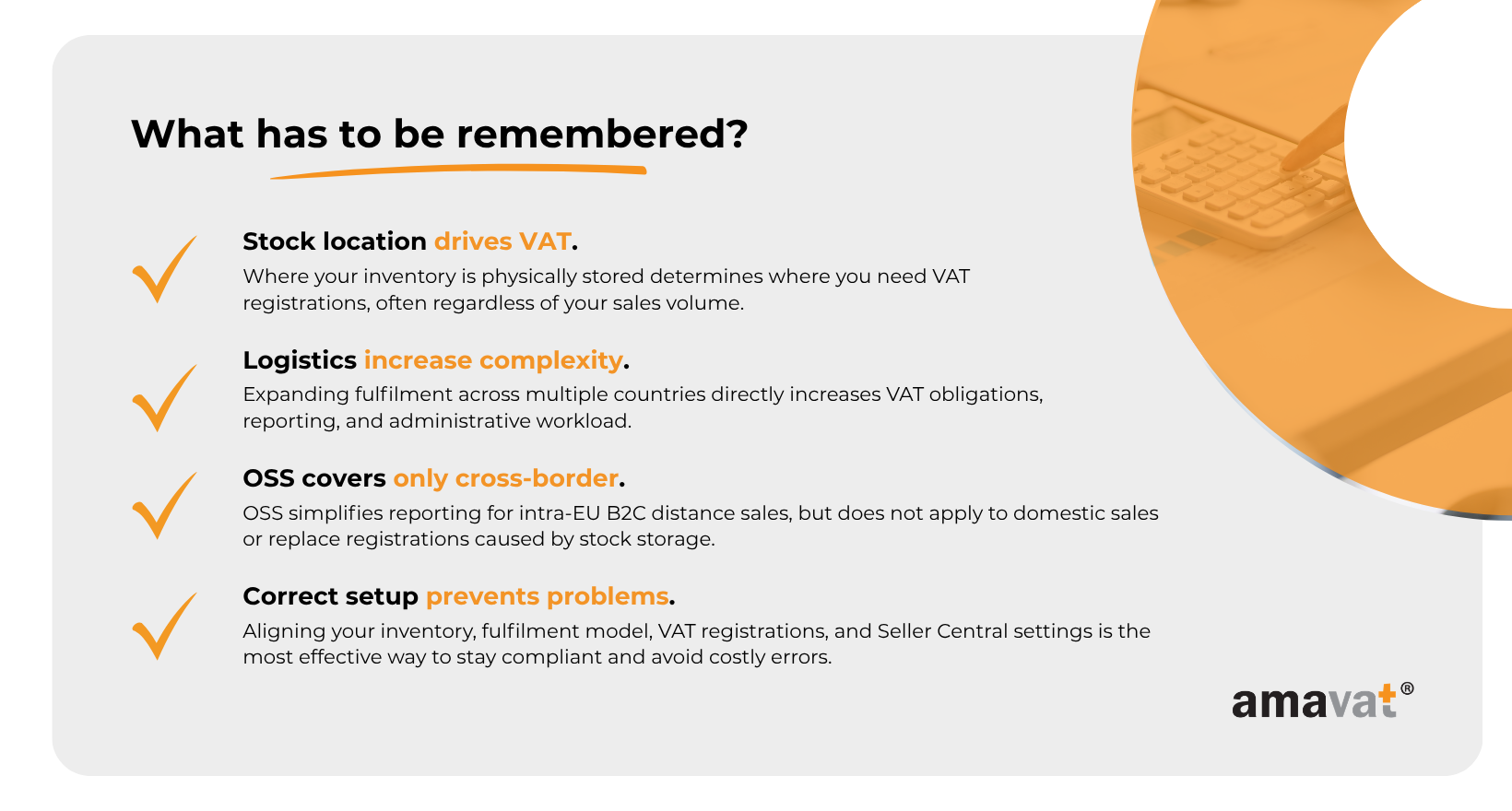

It’s worth keeping one thing in mind here. OSS helps with cross-border B2C distance sales, but it does not replace VAT registrations that are required because your stock is physically stored in another Member State. Those obligations still exist separately under current rules.

The third rule is one that often gets overlooked early on. Amazon charges VAT on its fees, including subscription, referral, and fulfilment costs. The way this VAT is applied depends on your VAT status, your location, and the tax details configured in your Seller Central account. It’s a separate layer from the VAT you charge your customers, but it still affects your overall tax position and needs to be handled correctly.

These rules won’t cover every edge case, but they give you a reliable mental model. If you understand them, you’re already ahead of most sellers trying to expand across the EU.

Simple Example to Anchor Understanding

Let’s make this real with a straightforward scenario.

Imagine you’re based in Poland and selling on Amazon using the European Fulfilment Network. All your stock is stored in Poland, and Amazon ships your products to customers in Germany and France.

From a VAT perspective, your inventory remains in Poland until the moment it is sold and dispatched. That means your primary VAT obligation is in Poland, where you are registered and filing returns.

As you start selling to customers in Germany and France, those sales become cross-border B2C transactions. Once your total cross-border sales within the EU exceed 10,000 EUR, you are generally required to apply the VAT rates of the customer’s country.

Instead of registering separately in Germany and France, you can use the OSS scheme through the EU country where you register for OSS, typically Poland. This allows you to report those cross-border sales in one place.

The key detail is that your stock never leaves Poland before the sale. Because of that, you typically do not need VAT registrations in Germany or France purely because you have customers there.

This is what a relatively clean setup looks like. One country of storage, one main VAT registration, and OSS handling the cross-border element. It’s often the starting point for sellers who want to keep things manageable while still reaching customers across the EU.

As your business grows and your logistics become more complex, your VAT setup will evolve as well. But the foundation stays the same. Everything comes back to where your stock is and where your customers are.

Fulfilment Models That Change Your VAT Obligations

If there’s one decision that quietly shapes your entire VAT setup on Amazon, it’s your fulfilment model.

Most sellers think about fulfilment in terms of speed, Prime eligibility, or shipping costs. That makes sense. But behind the scenes, your fulfilment choice is also deciding how many countries you’ll deal with from a VAT perspective, how many registrations you’ll need, and how complex your reporting becomes.

In simple terms, logistics and VAT are tightly connected. The more your stock moves across borders, the more your VAT obligations expand with it.

Let’s break down the three main setups Amazon sellers use in the EU, starting from the simplest and moving toward the most complex.

EFN (European Fulfilment Network): The Simplest Setup

The European Fulfilment Network, or EFN, is usually where most sellers begin—and for good reason. It keeps things relatively clean.

With EFN, you store your inventory in a single EU country. Amazon then ships your products from that one location to customers across other EU countries. Your stock stays in one place until a sale happens.

From a VAT perspective, this setup is about as straightforward as it gets.

You typically have a VAT registration in the country where your stock is stored. This becomes your primary VAT registration, where your domestic reporting takes place. As you begin selling to customers in other EU countries, those transactions are treated as cross-border B2C sales.

Once you exceed the EU-wide threshold, or choose to opt in earlier, you can use OSS to report those cross-border sales through the EU country where you are registered for OSS, usually your country of establishment.

As long as your stock remains in a single country, you generally avoid VAT registration obligations in other EU countries that would be triggered by storage. This is what keeps EFN relatively simple from a tax perspective.

That simplicity is exactly why many sellers start here. It allows you to reach customers across Europe without immediately stepping into a multi-country VAT setup.

Multi-Country Inventory / NAP: Scaling Comes With Complexity

As your business grows, faster delivery and local availability start to matter more. That’s where Multi-Country Inventory, often referred to as NAP, comes into play.

With this model, you choose to store your inventory in multiple Amazon fulfilment centres across different EU countries. Your products are positioned closer to customers, which can improve delivery times and conversion rates.

From a VAT perspective, this is where things become more demanding.

As soon as your stock is physically stored in another country, this will typically trigger a local VAT registration obligation there. In practice, this means registering in each country where your inventory is held.

At the same time, movements of your own stock between countries need to be reported. These are treated as intra-Community transfers of your own goods. In the country of dispatch, you report an intra-Community supply, and in the country of arrival, you report an intra-Community acquisition. Even though no sale takes place, these are VAT-reportable movements that must be included in your filings.

OSS still plays a role, but it’s important to understand its limits. OSS applies to cross-border B2C distance sales. However, when goods are sold from stock located within a country, those are domestic sales and must be reported in the local VAT return for that country.

This is where the structure changes. You’re no longer just managing cross-border sales from one location. You’re operating within multiple VAT jurisdictions, each with its own reporting obligations.

Pan-European FBA: Maximum Reach, Maximum VAT Complexity

Pan-European FBA takes this one step further.

Instead of choosing where your stock is stored, Amazon distributes your inventory across multiple EU countries automatically. The system is designed to optimise delivery speed by placing products closer to customers across Europe.

From a logistics perspective, it’s highly efficient. From a VAT perspective, it’s the most complex model.

Because your stock is stored in multiple countries, you will typically need VAT registrations in each country where that inventory is held. This is driven by a combination of local sales and intra-Community transfers of your own goods.

Each of these countries becomes its own VAT jurisdiction for your business. That means multiple VAT returns, multiple reporting timelines, and more administrative coordination.

Stock movements also become more frequent. Amazon may transfer your goods between countries as part of its internal optimisation, and each of these movements must be tracked and reported correctly.

OSS still applies to cross-border B2C sales, but its role becomes more limited in practice. In a Pan-European setup, many transactions become domestic sales from local stock, which must be reported through local VAT registrations rather than through OSS.

This is why Pan-European FBA is often seen as a trade-off. You gain operational efficiency and faster delivery, but you take on a significantly higher level of VAT complexity.

Quick Comparison: Choosing the Right Model

Looking at these models side by side makes the progression clear.

EFN keeps your setup lean. One country of stock, one primary VAT registration, and OSS handling cross-border B2C sales. It’s a low-complexity model that works well when you’re still building or want to keep things simple.

Multi-Country Inventory introduces a layer of expansion. You gain logistical advantages, but each additional country means a new VAT registration and additional reporting obligations. It’s a step into a more structured, multi-country setup.

Pan-European FBA pushes this to its full extent. Your inventory is spread across multiple countries, and your VAT obligations expand accordingly. You’re managing several VAT registrations, reporting stock movements, and handling domestic sales in multiple jurisdictions.

There’s no universal best choice here. It depends on your growth stage, your operational priorities, and how much complexity you’re ready to manage.

What matters most is understanding that your fulfilment strategy is not just an operational decision. It directly shapes your VAT structure. And getting that balance right early on can save you a lot of time, cost, and friction as your business grows.

When Do You Actually Need to Register for VAT?

This is the moment where things stop being theoretical and start becoming very real for your business.

Because up until now, VAT might feel like something you’ll “figure out later.” But registration obligations don’t wait for you to be ready. They’re triggered by specific actions—often small, operational decisions that don’t feel like tax decisions at all.

The tricky part is that many sellers assume VAT registration is tied mainly to revenue. In reality, for Amazon sellers in the EU, it’s much more about what you do than how much you sell.

Mandatory Triggers You Can’t Ignore

There are a few situations where VAT registration becomes very difficult to avoid. These are the core triggers that every Amazon seller operating in the EU should understand early on.

The first, and most important, is storing goods in a country.

The moment your inventory is physically present in another EU country, this will typically trigger a local VAT registration obligation, as the movement of goods creates a reportable intra-Community acquisition and enables local taxable sales.

For Amazon sellers, this usually happens through FBA, where stock is placed in fulfilment centres across different Member States.

It’s important to understand what’s really happening here. It’s not just the physical presence of goods that matters, but the fact that those goods have been moved across borders and are now available for sale locally. Under EU VAT rules, that combination creates reporting obligations that can’t be ignored.

The second trigger is importing goods into the EU.

If you’re bringing products into the EU from outside—whether from China, the UK, or the US—you will often need a VAT registration in the country of import, especially if you act as the importer of record and want to recover import VAT through a local VAT return.

The exact setup can vary depending on how your logistics and customs processes are structured. In some cases, different arrangements may apply, but for many Amazon sellers, import activity is closely linked to local VAT registration.

The third trigger is local VAT thresholds, although this plays a smaller role in most Amazon setups.

In traditional business models, VAT registration thresholds depend on your turnover within a country. But in many Amazon scenarios, stock-related obligations arise before turnover thresholds become relevant. By the time you reach a threshold, you may already have a VAT registration requirement due to how your inventory is structured.

So while thresholds still exist, they are rarely the starting point when determining VAT obligations in an FBA-driven business.

The Most Important Trigger: Stock Location

If there’s one concept to take away from this entire guide, it’s this: stock location drives VAT obligations more than anything else.

It’s easy to think in terms of sales—where your customers are, how much you’re selling—but tax authorities are just as focused on where your goods physically sit before the sale happens.

This is where Amazon FBA changes the game.

When you send stock to a fulfilment centre in another EU country, that action is not just logistical. From a VAT perspective, it is usually treated as a movement of your own goods between Member States. That movement is VAT-reportable and typically requires you to be identified for VAT in the destination country.

In other words, thresholds don’t protect you here. Even if you haven’t made any sales in that country yet, the act of placing stock there can be enough to trigger a registration requirement.

A simple example makes this clear.

Imagine you’re based in Poland and decide to send part of your inventory to an Amazon warehouse in France to improve delivery times. You haven’t sold anything to French customers yet. Your listings are live, but sales haven’t started.

From a business perspective, it might feel like nothing has happened yet.

From a VAT perspective, something very important just did.

Your stock has moved from Poland to France. That movement is typically treated as an intra-Community transfer of your own goods. As a result, you will typically need a VAT registration in France to report the intra-Community acquisition of your goods and any subsequent domestic sales.

This is why so many sellers run into VAT issues without realising it. The trigger isn’t always revenue. It’s often logistics.

Once you understand that, things start to click. Every time you decide where your stock goes, you’re also shaping your VAT footprint across Europe.

The 10,000 EUR Threshold and OSS Explained Clearly

This is probably the most talked-about rule in EU VAT for e-commerce—and also one of the most misunderstood.

A lot of sellers hear about the 10,000 EUR threshold and assume it’s some kind of safety zone. Stay below it, and you’re fine. Go above it, and things get complicated.

The reality is more nuanced.

The threshold only applies to specific types of transactions, and it works alongside other VAT rules, not instead of them. If you understand where it fits, it becomes a useful tool. If you misunderstand it, it can give you a false sense of security.

What Happens Below the Threshold

If your total intra-EU distance sales to consumers, together with certain digital services, stay below 10,000 EUR per year, you’re allowed to keep things relatively simple—under specific conditions.

In this case, you can generally charge VAT based on your country of establishment, provided your business is established in only one EU Member State and does not have a fixed establishment elsewhere.

So if you’re based in Poland, you apply Polish VAT rates even when selling to customers in Germany, France, or other EU countries.

These sales are then reported in your domestic VAT return, just like local sales. There’s no immediate need to apply foreign VAT rates or register in other countries purely because your customers are located there.

But there’s an important detail that often gets overlooked.

This threshold only applies to a defined category of transactions, and it does not override other VAT triggers. If you store stock in another country or create other taxable activities there, those obligations still apply regardless of your turnover level.

Even if you remain below the threshold, you can choose to use OSS voluntarily. Some sellers do this early to simplify pricing across countries or to prepare for growth. Once you opt in, that choice generally applies for at least two calendar years.

So being below 10,000 EUR gives you flexibility, but it doesn’t remove the need to think ahead.

What Happens Above the Threshold

Once your total qualifying cross-border sales exceed 10,000 EUR, measured across the current and previous calendar year, the rules shift.

At that point, VAT is generally due in the country where the customer is located. This is known as the destination principle.

In practice, this means you must apply the VAT rate of the customer’s country when making cross-border B2C sales. Your pricing, margins, and reporting all start to vary depending on where your customers are based.

You then have two main ways to handle this.

One option is to register for VAT in each country where VAT is due on your sales and report those transactions locally. While this approach is legally valid, it quickly becomes difficult to manage as your business expands across multiple markets.

The more practical route for most sellers is to use the One Stop Shop.

With OSS, you can report intra-Community distance sales of goods through a single VAT return submitted in your Member State of identification, usually your country of establishment. You still apply the correct VAT rates for each destination country, but you avoid having to file separate returns in each one.

OSS doesn’t change how VAT is calculated. It changes how it’s reported and paid. And that’s what makes it such a useful tool as your cross-border sales grow.

What OSS Does—and What It Does NOT Do

OSS is powerful, but it’s not a complete solution to all VAT challenges.

What it does is simplify the reporting of intra-Community distance sales of goods to consumers. It allows you to declare those cross-border B2C transactions through a single system instead of registering in multiple countries solely because of those sales.

But it’s important to understand where its limits are.

OSS does not apply to all types of transactions.

If you sell goods from stock located within a country to customers in that same country, those are domestic sales. They must be reported in the local VAT return for that country, not through OSS.

And just as importantly, OSS does not replace VAT registrations that are required because your stock is physically stored in another Member State. If you hold inventory in a country, you will still typically need a local VAT registration there due to stock movements and domestic sales.

The easiest way to think about it is this.

OSS governs where VAT is reported for cross-border sales. It does not affect VAT obligations arising from stock location.

Once you clearly separate those two layers—customer location and stock location—the whole system becomes much easier to understand and manage.

Setting Up VAT in Amazon Seller Central (Step-by-Step)

This is where theory meets execution.

You can understand VAT rules perfectly, but if your Amazon account isn’t configured correctly, things will still go wrong. Missing VAT numbers, incorrect settings, or ignored reports can quickly turn into reporting errors, pricing issues, or compliance risks.

The good news is that Seller Central gives you the tools you need. The bad news is that it doesn’t guarantee you’ll use them correctly.

Think of this section as your operational layer—how to make sure your VAT setup inside Amazon actually matches your real-world obligations.

Adding VAT Numbers

The first step is making sure your VAT registrations are properly reflected in your Seller Central account.

Inside your tax settings, Amazon allows you to add VAT identification numbers for each EU country where you are registered. This is not just administrative. These numbers directly influence how Amazon treats your transactions and calculates VAT on its services.

Each VAT number should match a country where you genuinely have a registration. Adding a VAT number “just in case” or leaving one out can create inconsistencies between your actual obligations and what Amazon assumes about your business.

Once your VAT numbers are in place, Amazon uses them to determine things like invoice logic, VAT treatment on fees, and how transactions are classified and presented in your account data.

This step is simple on the surface, but it’s foundational. If your VAT numbers are wrong or incomplete, everything built on top of them becomes unreliable.

Enabling VAT Calculation Services

Amazon offers a feature called VAT Calculation Services, and for most sellers, it’s one of the most useful tools available.

When enabled, Amazon automatically calculates VAT on your sales based on your settings and the data in your account. It also generates invoices that are generally VAT-compliant, depending on how your configuration is set up.

This becomes especially important once you start applying different VAT rates depending on the customer’s country. Manually managing this across multiple markets is not realistic at scale.

That said, automation doesn’t mean accuracy by default.

Amazon does not validate whether your VAT setup is legally correct. It simply applies the logic based on the inputs you provide. If your VAT registrations, fulfilment settings, or tax configuration are wrong, the calculated VAT and generated invoices may also be incorrect.

So while VAT Calculation Services can save you time, it should be treated as a support tool, not a substitute for understanding your VAT obligations.

Configuring Fulfilment Settings

This is one of the most overlooked areas when it comes to VAT—and one of the most important.

Your fulfilment settings determine where Amazon is allowed to store and move your inventory. And as you’ve seen earlier, stock location is one of the main drivers of VAT obligations.

If you enable programmes like Pan-European FBA or Multi-Country Inventory without fully understanding the implications, you may end up with stock in countries where you are not VAT registered.

This creates a mismatch between your logistics setup and your tax compliance.

Inside Seller Central, you can control where your inventory is stored and which fulfilment programmes you participate in. These settings should always align with your VAT registrations.

In practical terms, that means you should know exactly which countries Amazon is allowed to use for your stock—and make sure you are VAT registered in all countries where Amazon may store your inventory, where required under VAT rules.

There’s one more thing many sellers don’t realise at the beginning.

In some fulfilment setups, Amazon may move your inventory between countries as part of its logistics optimisation. This can happen even if you didn’t explicitly choose those locations. As a result, VAT obligations can arise in countries you didn’t originally plan for.

That’s why it’s important not only to configure your settings, but also to monitor where your stock is actually stored over time.

Downloading VAT Reports

Amazon generates a large amount of data, but knowing which reports matter makes all the difference.

Two of the most important ones for VAT purposes are the VAT Transaction Report and the Tax Document Library.

The VAT Transaction Report includes detailed data on your sales, refunds, and stock movements across countries. However, this data often requires reconciliation before it can be used for VAT reporting, especially in more complex, multi-country setups.

The Tax Document Library contains invoices and official documents generated within your account, including documents related to Amazon fees and customer invoices.

Downloading these reports regularly is essential. VAT reporting is based on actual transaction data, and gaps or inconsistencies can lead to incorrect filings.

Most experienced sellers build a routine around this—monthly or even more frequently—to keep everything aligned and ready for reporting.

Optional: Using VAT Services Providers

At some point, many sellers realise that managing VAT across multiple countries is not something they want to handle alone.

Amazon offers its own solution, often referred to as VAT Services on Amazon, which can help with VAT registrations and filings in selected EU countries. It’s integrated into Seller Central and can be convenient, although the scope and level of support may be more limited compared to specialised providers.

There are also third-party VAT providers that focus specifically on e-commerce and Amazon sellers. These companies typically offer broader support, including multi-country registrations, ongoing filings, and communication with tax authorities in different jurisdictions.

The right choice depends on how complex your setup is.

If you’re operating in one or two countries, Amazon’s solution might be enough. If you’re scaling across multiple markets or using more advanced fulfilment models, a specialised provider can offer more flexibility and reduce the risk of mistakes.

At the end of the day, VAT compliance in the EU is not just about having the right tools. It’s about making sure those tools are set up and used correctly as your business evolves.

How to Report VAT Across Multiple EU Countries

This is the part where most sellers start to feel overwhelmed—and where most articles fall short.

Because understanding when you need a VAT registration is one thing. Actually reporting everything correctly across multiple countries is something else entirely.

Once you move beyond a single-country setup, VAT reporting becomes a system. Different types of transactions go into different reports, often in different countries, sometimes at the same time. And if you mix them up, things don’t just get messy—they become incorrect.

The key is to stop thinking of VAT as one report and start seeing it as a structure made up of several layers. Each layer handles a specific type of transaction.

Once you understand those layers, everything becomes much more manageable.

Domestic VAT Returns (Per Country)

Every country where you are VAT registered becomes its own reporting environment.

A domestic VAT return in a given country is where you report transactions that are considered local to that country. This includes sales made from stock located there, as well as other taxable activities connected to that jurisdiction.

If you hold stock in Germany, for example, you will have a German VAT return. If you also store goods in Italy, you will have a separate Italian VAT return. Each one stands on its own.

Within these returns, you typically report domestic sales to consumers and businesses, meaning transactions where the goods are dispatched and delivered within the same country. These are local supplies and must be handled under that country’s VAT rules.

You also report intra-Community acquisitions, imports, and related input VAT deductions where applicable. If you act as the importer of record or receive goods from another Member State, these entries become part of your local VAT reporting.

Both B2C and B2B transactions are included, although they may be treated differently depending on the nature of the sale and the status of the customer.

The important thing to understand is that domestic VAT returns are not optional or interchangeable. If you are registered in a country, you are expected to report all relevant local activity there—regardless of whether you are also using OSS or operating in other markets.

Intra-Community Transfers (Stock Movements)

This is one of the most misunderstood parts of EU VAT, and also one of the most important for Amazon sellers.

When you move your own goods from one EU country to another, this is not ignored for VAT purposes. It is treated as a reportable intra-Community transaction, even though there is no external customer involved.

In the country where the goods are dispatched, you report an intra-Community supply of your own goods, often referred to as a WDT. In many cases, it is zero-rated, provided the relevant conditions are met, such as valid VAT identification and proper documentation.

In the country where the goods arrive, you report an intra-Community acquisition, known as a WNT. This reflects the fact that the goods have entered that country and are now part of your local stock.

These two entries are linked. One reflects the departure, the other the arrival.

For Amazon sellers using FBA, this becomes a regular occurrence. Every time inventory is moved between countries, whether by you or by Amazon, these movements must be captured and reported for VAT purposes.

This is also one of the main reasons VAT registrations are required in multiple countries. Without a local VAT number, you cannot properly report the arrival of goods or account for subsequent domestic sales.

OSS Returns

The One Stop Shop adds another layer to your VAT reporting, but it only applies to a specific category of transactions.

OSS is used for intra-Community distance sales of goods to consumers. In simple terms, this means cross-border B2C sales where goods are shipped from one EU country to another.

These transactions are not reported in a domestic VAT return in the destination country, but instead through OSS, which is submitted in your Member State of identification.

Within the OSS return, you break down your sales by country of consumption and apply the correct VAT rates for each of those countries. The tax is then distributed to the relevant Member States through the OSS system.

It’s important to keep the boundaries clear.

If a sale is cross-border and qualifies as a distance sale, it goes into OSS. If a sale is domestic—meaning the goods are shipped and delivered within the same country—it must be reported in the local VAT return for that country.

OSS simplifies reporting, but only for the cross-border layer. It does not replace domestic VAT returns, and it does not apply to stock movements.

EC Sales Lists / Recapitulative Statements

In addition to VAT returns, there is another reporting obligation that often comes into play: EC Sales Lists, also known as recapitulative statements.

These are used to report intra-Community supplies made to VAT-registered customers in other EU countries. If you sell goods to a business customer in another Member State and apply the reverse charge, that transaction is typically included in an EC Sales List.

In many cases, intra-Community transfers of your own goods must also be reported in EC Sales Lists, depending on local requirements.

The purpose of these statements is to allow tax authorities to cross-check transactions between Member States. What you report as a supply in one country should match what is reported as an acquisition in another.

Not every seller will encounter EC Sales Lists immediately, but they typically become relevant once you perform cross-border B2B transactions or stock transfers.

Real Example Scenario

Let’s bring all of this together with a practical example.

Imagine you’re based in Poland and using an FBA setup where part of your stock is moved to Italy.

First, the stock transfer itself.

When your goods move from Poland to Italy, this is treated as an intra-Community transfer of your own goods. In Poland, you report an intra-Community supply. In Italy, you report an intra-Community acquisition.

This happens regardless of whether you have made any sales yet. The movement alone creates reporting obligations in both countries.

Next, the sales.

Once your products are stored in Italy and sold to Italian customers, those transactions are considered domestic Italian sales. They are reported in your Italian VAT return and taxed using Italian VAT rates.

If you also sell to customers in another EU country from your Italian stock—for example, shipping from Italy to Spain—those transactions may qualify as intra-Community distance sales and can typically be reported through OSS.

So in this one scenario, you have multiple layers working together.

A stock movement reported in two countries. Domestic sales reported locally in Italy. And cross-border sales reported through OSS.

This is why VAT reporting across multiple EU countries can feel complex. It’s not one system—it’s several systems running in parallel.

But once you understand which transactions belong where, it becomes a structured process rather than a guessing game.

Special Considerations for Non-EU Sellers

If you’re selling on Amazon in the EU but your business is based outside the EU, the core VAT logic remains the same, but additional rules and obligations apply.

You’re still dealing with the same fundamentals—where your stock is located and where your customers are. But on top of that, you now have customs procedures, import VAT, and marketplace-specific rules that add extra layers of complexity.

In practice, this means more moving parts, more decisions to get right, and more risk if something is set up incorrectly.

Importing Goods Into the EU

For non-EU sellers, importing goods is usually the starting point of the entire VAT chain.

Before you can sell anything in the EU, your products need to enter the EU customs territory. This process involves customs declarations, potential duties, and import VAT. To operate within this system, you generally need an EORI number, which acts as your identification for customs purposes across the EU.

One of the most important decisions here is determining who acts as the importer of record.

This role carries significant responsibility. The importer of record is responsible for customs declarations, payment of import VAT, and ensuring compliance at the border. It also directly affects whether import VAT can be recovered and whether a local VAT registration is required.

When goods are imported, VAT is typically due in the country of entry. If you act as the importer of record, you will often need a VAT registration in that country, especially if you want to recover import VAT through a local VAT return or make local sales from that stock.

However, the exact setup can vary depending on how your logistics and customs arrangements are structured. Different models, such as indirect representation or postponed import VAT schemes, can change how and where VAT is handled.

Deemed Supplier Rules (Amazon’s Role)

One of the key developments in EU VAT is the introduction of deemed supplier rules for online marketplaces like Amazon.

In certain situations, Amazon is treated as the supplier for VAT purposes. This means Amazon becomes responsible for collecting and remitting VAT for those specific transactions, even though you remain the underlying seller commercially.

This typically applies in cases such as distance sales of imported goods with a value not exceeding 150 EUR, and sales by non-EU sellers to EU consumers where the goods are already located within the EU.

From a seller’s perspective, this can simplify part of the VAT process. Amazon handles VAT collection on those transactions, which reduces your direct reporting obligations for that specific flow.

But it’s important not to overgeneralise.

These rules apply only to defined scenarios. They do not cover your entire business. You may still have VAT obligations related to importing goods, storing stock in EU warehouses, or making other types of sales.

So while Amazon takes over VAT handling in certain cases, you still need to understand which transactions fall inside that scope and which remain your responsibility.

OSS and IOSS for Non-EU Sellers

Non-EU sellers can still use simplified VAT reporting schemes, but the structure is slightly different compared to EU-based businesses.

For intra-EU sales, non-EU businesses can access OSS by registering in an EU Member State. Depending on the setup, this may involve the Union or non-Union scheme. This allows you to report eligible cross-border B2C sales through a single return instead of registering in multiple countries solely for those transactions.

For goods imported from outside the EU, there is also the Import One Stop Shop, or IOSS.

IOSS applies to distance sales of goods with a value not exceeding 150 EUR. It allows VAT to be collected at the point of sale, which typically removes the need to pay import VAT at the border and helps ensure smoother customs clearance.

Non-EU sellers can use IOSS, but in most cases, they must appoint an intermediary established in the EU to access the scheme.

Both OSS and IOSS are designed to simplify reporting, but they only apply to specific transaction types. They do not replace VAT registrations required due to stock storage, imports, or other local activities.

Why Compliance Is More Complex (and Risky)

For non-EU sellers, VAT is only one part of the equation. Customs and VAT operate side by side, and they are closely connected.

Every import involves customs classification, valuation, and documentation. At the same time, VAT must be handled correctly at import and during subsequent sales.

These systems don’t operate independently. A mistake in customs—such as incorrect valuation or classification—can affect your VAT position. Likewise, an incorrect VAT setup can lead to issues with customs clearance or recovery of import VAT.

On top of that, non-EU sellers often rely on intermediaries, deal with multiple authorities, and navigate slightly different administrative practices across Member States.

This creates more points where things can go wrong.

A misalignment between your customs setup, importer-of-record structure, and VAT registrations can lead to delays, blocked shipments, or VAT that cannot be recovered.

That’s why for non-EU sellers, VAT compliance isn’t just about filing returns. It’s about building a structure where logistics, customs, and tax all work together.

Getting that structure right early doesn’t just reduce risk—it makes scaling across the EU significantly smoother.

Practical Checklist: Staying VAT-Compliant on Amazon EU

By now, you’ve seen how VAT on Amazon isn’t one single rule—it’s a system that reacts to how your business operates.

This section is about turning all of that into something practical. Not theory, not edge cases—just the core things you need to stay on top of if you want to avoid problems as you grow.

Think of it less like a checklist you go through once, and more like a routine you build into how you run your business.

Start With Your Inventory, Not Your Sales

If there’s one place to begin, it’s your stock.

You need a clear, up-to-date view of where your inventory is physically stored across the EU. Not where you think it is, not where you originally sent it—but where it actually sits right now.

This matters because your VAT obligations follow your inventory. If your stock is in Germany, Italy, or Spain, those countries will typically require you to be VAT registered there.

And this is where many sellers slip up.

Amazon may move your inventory between countries automatically, which can create VAT obligations even if you did not actively choose those locations. That means your VAT footprint can change without you making a conscious decision.

So mapping your inventory isn’t something you do once—it’s something you monitor regularly.

Understand Where Your Customers Are—and What That Means

The second layer is your customers.

You should have a clear picture of where your buyers are located and how your sales are distributed across EU countries. This isn’t just useful for marketing or logistics—it directly affects how VAT is calculated and reported.

Once your total intra-EU distance sales exceed the 10,000 EUR threshold across the current and previous year, VAT is generally due in the customer’s country. That changes how you price your products and how you report those sales.

Even before reaching that threshold, tracking this early helps you decide when to move to OSS and avoids sudden shifts in your reporting obligations.

Choose Your Fulfilment Model Deliberately

Your fulfilment setup is one of the biggest drivers of VAT complexity, so it should always be a conscious decision—not just a default setting.

If you keep your stock in one country, your VAT setup stays relatively simple. As soon as you expand into multiple countries or enable programmes like Pan-European FBA, your VAT obligations expand with it.

There’s no single right choice here, but there is always a trade-off.

Faster delivery and better customer experience usually mean more VAT registrations, more reporting, and more coordination. Simpler setups mean fewer obligations, but potentially slower expansion.

The key is making sure your VAT setup evolves together with your fulfilment strategy—not after it.

Make Sure Your VAT Registrations Match Reality

At any point in time, you should be able to answer a simple question: in which countries am I required to be VAT registered?

This usually includes your home country, plus every country where your stock is stored, where you import goods—particularly if you act as the importer of record or need to recover import VAT—and where other VAT-triggering activities take place.

If you’re using OSS, you’ll also have a country where you are registered for that scheme, known as your Member State of identification.

What matters most is alignment.

Your registrations should reflect your actual operations. If there’s a mismatch—stock in a country without a VAT number, or registrations that don’t match your activity—that’s where problems tend to start.

It’s also worth noting that a VAT number without corresponding activity can still create reporting obligations, such as nil returns, so these should be monitored as well.

Keep Seller Central Aligned With Your VAT Setup

Your Amazon account needs to reflect your real-world VAT structure.

That means your VAT numbers, fulfilment settings, and tax configuration should all be consistent with how your business actually operates.

If you’re registered in multiple countries, those VAT numbers should be correctly entered. If you’re using specific fulfilment programmes, your settings should match where you are allowed—and prepared—to hold stock.

It’s also important to review these settings regularly. As your logistics evolve, your VAT setup needs to stay aligned with it.

Build a Routine Around VAT Data

VAT reporting depends on accurate data, and on Amazon, that data lives in your reports.

Downloading and reviewing your VAT Transaction Report and related documents shouldn’t be something you do only at the end of a quarter. It works much better as a regular habit.

This allows you to spot inconsistencies early, understand how your transactions are being recorded, and avoid surprises when it’s time to file returns.

In more complex setups, this data often needs to be reconciled before it’s usable. That’s normal. What matters is that you’re not discovering issues at the last minute.

Make Sure Transactions Are Classified Correctly

One of the most common sources of VAT errors is misclassification.

Every transaction needs to be correctly identified as a domestic sale, an intra-Community distance sale, or a transfer of your own goods between countries.

If these categories are mixed up, VAT may be reported in the wrong place or not reported at all. This can create inconsistencies between countries and increase the risk of audits or corrections later.

Having a clear understanding of how your transactions are classified—and making sure your data reflects that—is essential for accurate reporting.

Stay on Top of Filing Deadlines

Each country where you are VAT registered will have its own filing deadlines and reporting cycles.

Missing a deadline can lead to penalties, even if your VAT calculations are correct. This is especially important in multi-country setups, where you may be dealing with several reporting timelines at once.

Building a calendar of deadlines and keeping track of filing obligations is a simple step that can prevent unnecessary issues.

Don’t Try to Do Everything Alone

At a certain point, VAT stops being something you can comfortably manage on your own—especially if you’re operating across multiple countries.

Working with VAT compliance specialists can take a lot of pressure off. Whether it’s Amazon’s own VAT services or a third-party provider, having someone who understands multi-country reporting, local requirements, and communication with tax authorities can make a big difference.

This isn’t just about saving time. It’s about reducing risk.

Because the more your business grows, the more expensive mistakes can become.

The Bigger Picture

If you step back, all of this comes down to one idea.

VAT compliance isn’t a separate task you handle occasionally. It’s part of how your business operates day to day.

Your inventory decisions, your fulfilment model, your pricing, and your reporting are all connected. When those pieces are aligned, VAT becomes manageable.

When they’re not, it quickly turns into friction.

The goal isn’t perfection. It’s control.

Conclusion: Simplify First, Scale Second

If there’s one idea to take away from this entire guide, it’s this: VAT complexity doesn’t come from selling more—it comes from operating in more places.

The moment your logistics expand across borders, your VAT obligations expand with them. More warehouses mean more registrations. More stock movements mean more reporting. More local sales mean more returns to file.

That’s why VAT on Amazon can feel overwhelming. Not because it’s random, but because it scales with your setup.

Once you see that connection clearly, things start to make more sense.

VAT Complexity Follows Your Logistics

It’s easy to think of VAT as something separate from your operations. But in reality, it’s directly tied to how your business runs day to day.

Every fulfilment decision you make—where you store stock, how you ship orders, which Amazon programmes you enable—has a tax consequence behind it.

Keep your logistics simple, and your VAT structure stays manageable. Expand across multiple countries, and your VAT setup becomes more complex to match.

This isn’t a problem. It’s just a trade-off.

And like any trade-off in business, it’s something you want to control, not stumble into.

Start Simple, Then Scale With Intention

For most sellers, the smartest approach is to start with a setup that keeps things lean.

Using a single-country storage model, combined with OSS for cross-border B2C sales, gives you access to selling across the entire EU market without immediately stepping into multi-country VAT compliance. It’s a clean, controlled way to grow.

As your business scales and you start thinking about faster delivery, better conversion rates, and local availability, expanding into multi-country fulfilment or Pan-European FBA can make sense.

But that move should be intentional.

By the time you get there, you want to understand what changes from a VAT perspective. More registrations, more reporting layers, more coordination. It’s not something to avoid—it’s something to prepare for.

Scaling works best when your tax structure grows with your logistics, not behind it.

VAT Is Manageable With the Right Structure

At first glance, EU VAT can feel like a maze. Different countries, different rules, different reports—it’s easy to assume it’s too complex to fully get under control.

But once you break it down, the system becomes much more structured.

Stock location drives where you register. Customer location drives how you charge VAT. Transaction type determines where you report it. Tools like OSS simplify specific parts of the process. And platforms like Amazon give you the data to make it all work.

It’s not simple, but it is logical.

And with the right setup, the right habits, and the right support when needed, VAT becomes structured and manageable—not overwhelming.

If you keep your inventory, fulfilment setup, and VAT registrations aligned, you’ll avoid most of the common problems sellers run into as they scale across the EU.