Amazon FBA VAT Declaration for International Sales – A Step-by-Step Guide to Reporting Sales (2026)

Spis treści

This is where many young EU entrepreneurs get caught out. The business starts lean: a few products, one marketplace, maybe stock in one country. Then Amazon offers Pan-European FBA, sales pick up in Germany, France, Spain, Italy, Poland, and suddenly your “simple” online store has VAT touchpoints across several tax systems. The tricky part is that VAT is not only about where your customer lives. It is also about where your inventory is stored, where it moves, who buys it, who collects the tax, and which return needs to include the transaction. Amazon gives you useful data, but it does not replace your responsibility to understand what that data means.

Your responsibility as the seller does not disappear

The key thing to understand is this: Amazon can support VAT reporting, but it does not become your accountant, tax adviser, or legal shield. As the seller, you are still responsible for knowing where you need a VAT number, which sales belong in a local VAT return, which sales can go through OSS, and which transactions Amazon has already handled under marketplace rules. If your stock is stored in another country, that alone can create a VAT registration obligation, even if your sales are still small. If goods move between fulfilment centres, those movements may also need to be recorded and reported, even though no customer has bought anything at that moment.

This guide is written for sellers who want to understand the process without drowning in tax jargon. We will look at where you may need to register for VAT, how to prepare your Amazon data before filing, and how VAT returns usually work for EU and UK FBA activity. The goal is not to turn you into a tax specialist overnight, but to give you a clear map of the system so you know what to check, what to ask your accountant, and where the biggest risks usually sit. Whether you are an EU-based seller, a non-EU entrepreneur using European warehouses, or a growing brand using Pan-EU FBA, the same basic rule applies: VAT follows your stock, your sales, and your reporting setup.

VAT Basics for Amazon FBA in 2026

Core VAT rules every seller must understand

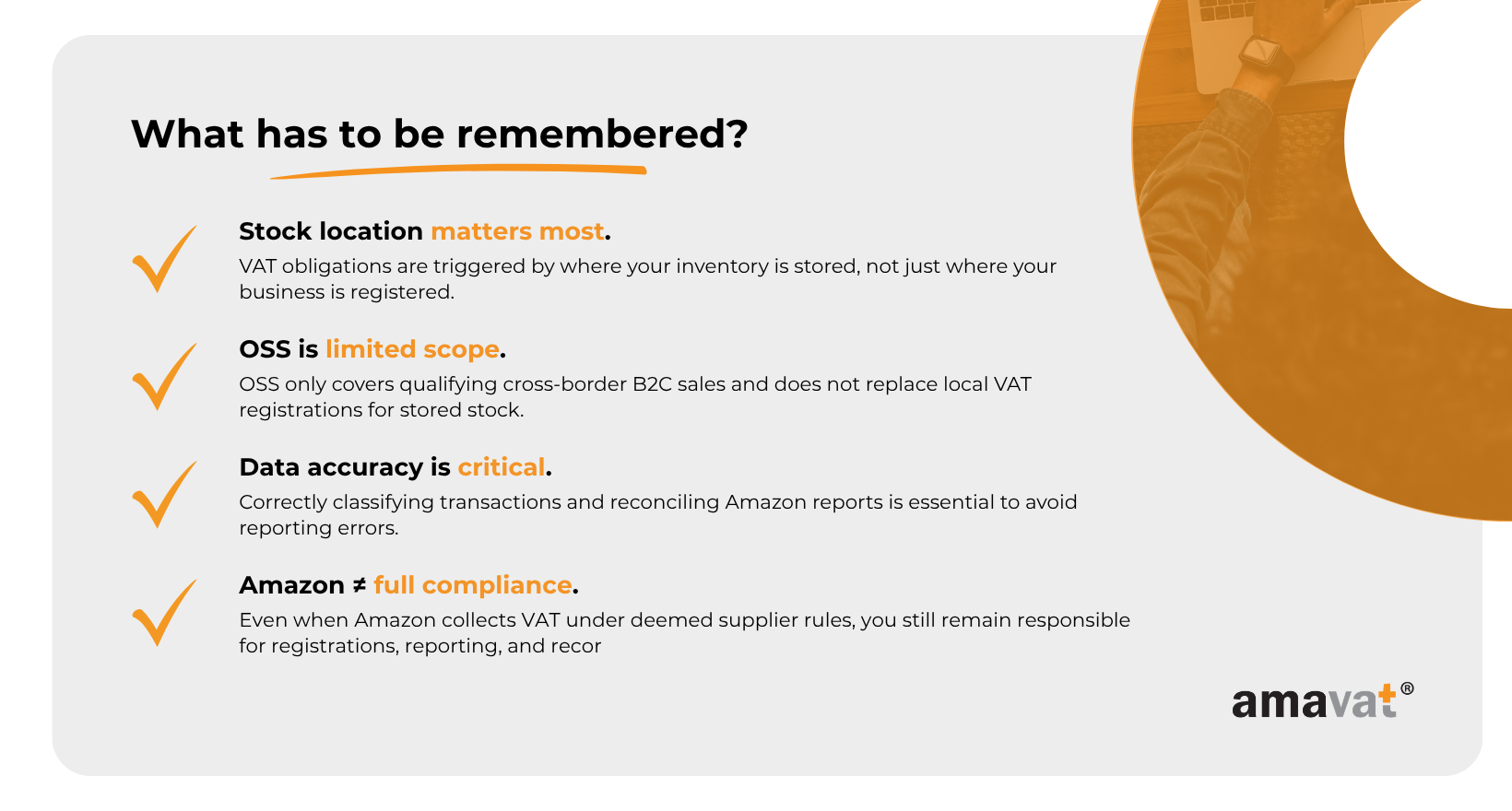

When you sell through Amazon FBA, VAT is not driven only by where your customers are. The real trigger is where your inventory physically sits. The moment your products are stored in a warehouse in another country, even if it is just a small batch, you are usually creating a VAT obligation there. This is why many sellers are surprised when they expand into Pan-EU FBA and suddenly need registrations in multiple countries. It does not matter if you have sold ten units or ten thousand. From a VAT perspective, storage equals presence, and presence often means registration and reporting.

It helps to think of VAT in three layers that can overlap depending on how your business operates. Domestic VAT applies when goods are sold and delivered within the same country, usually from local stock to local customers. Cross-border VAT comes into play when you sell to customers in other EU countries, especially in B2C scenarios where distance selling rules apply. Then there is import VAT, which appears when goods enter a country from outside its borders, often when you ship products from China or another non-EU location into an EU or UK warehouse. These categories are not separate boxes but parts of one system, and a single business can deal with all three at the same time if it stores, moves, and sells goods internationally.

OSS (One Stop Shop) explained

The One Stop Shop system was designed to simplify VAT for cross-border sales within the EU, but it is often misunderstood. In simple terms, OSS allows you to report VAT on qualifying B2C sales to customers in other EU countries through a single quarterly return, submitted in your country of registration. This becomes relevant once your total EU cross-border B2C sales and certain services exceed 10,000 euros per year. Below that threshold, many EU sellers can usually continue applying their home country VAT rules, but once they cross it, they generally need to either use OSS or deal with VAT obligations in the customer’s country.

OSS does not remove the need for local VAT registrations where stock is stored. Domestic sales from that stock, stock transfers, imports and B2B transactions must generally be handled outside OSS. However, OSS can still be used for qualifying B2C cross-border sales where goods are shipped from one EU country to consumers in another EU country. This is why OSS and local VAT registrations often exist side by side for Amazon FBA sellers. OSS is useful, but it is not a magic button that covers every sale, every warehouse, or every movement of goods inside your Amazon setup.

Marketplace VAT rules and Amazon as a deemed supplier

Over the past few years, marketplace rules have introduced the concept of the “deemed supplier,” which changes how VAT is collected in certain situations. In practice, this means that Amazon may step in and collect VAT directly from the customer on specific transactions, especially for low-value goods or certain cross-border sales. From the buyer’s perspective, everything looks seamless. From the seller’s perspective, it can feel like Amazon has taken over the VAT responsibility. But that is only partially true.

Even when Amazon collects VAT, your obligations do not disappear. You still need to maintain VAT registrations where required, especially in countries where your stock is stored. You also need to correctly record these transactions in your accounting, because they are often treated as sales to Amazon rather than directly to the end customer. On top of that, proper reporting and documentation remain essential. Tax authorities expect consistent records that match your filings, your Amazon reports, and your inventory movements. So while marketplace rules reduce some of the operational burden, they do not remove the need for a clear VAT setup. If anything, they add another layer that you need to understand and track properly as your business grows.

Important customs change from 1 July 2026: The EU abolished the €150 customs duty exemption for low-value imports. From 1 July 2026, a temporary flat-rate customs duty of €3 per item applies to all imported e-commerce consignments valued at €150 or less, including those reported through IOSS. This applies in addition to import VAT and will remain in place until 1 July 2028, when the broader EU Customs Reform takes effect. For Amazon FBA sellers shipping goods from outside the EU directly to EU consumers, this means IOSS alone no longer covers the full tax burden at the point of sale — sellers need to factor in the €3 customs duty when pricing and communicating with customers.

Where You Must Register for VAT (2026 Rules)

General VAT registration rules

When you run an Amazon FBA business in the EU, VAT registration is less about where your company is based and more about where your activity actually happens. Your home country is usually the starting point. If you are established in an EU country and begin selling goods, you typically need a local VAT number once your business becomes taxable there. This covers your domestic sales, local expenses, and the core reporting tied to your business. For many sellers, this is the foundation that everything else builds on, including OSS if cross-border sales start to grow.

Things become more complex the moment your products enter Amazon’s wider fulfilment network. Storage is one of the main triggers. If your stock is held in another EU country, even if Amazon moves it automatically as part of a fulfilment program, local VAT registration is usually still required there. It does not matter whether you actively chose that warehouse or not. From a tax perspective, the goods are physically present, and that presence creates obligations. At the same time, cross-border B2C sales introduce another layer. Once you exceed the 10,000 euro threshold for EU-wide distance sales, you need to consider OSS or local registrations in customer countries. OSS may still help with eligible cross-border B2C sales, but it does not cover domestic sales from local stock, stock transfers, imports or B2B sales. In practice, this means many sellers operate with a mix of local VAT registrations and OSS, depending on how their logistics are structured.

VAT for non-EU sellers

For non-EU entrepreneurs, VAT obligations in Europe tend to start earlier and move faster. In many cases, there is no meaningful threshold that delays registration, especially when using Amazon FBA. If you import goods into an EU country and store them in a warehouse, this alone can create a requirement to register for VAT, sometimes even before your first sale takes place. Importation and storage are treated as taxable activities, which means the system expects you to be registered and reporting from the start rather than once revenue reaches a certain level.

It is also important to understand the limits of marketplace involvement. While Amazon may collect VAT on certain B2C transactions under marketplace rules, this does not remove your broader obligations as a seller. You may still need VAT registrations in countries where your stock is stored, and you remain responsible for reporting stock movements, handling imports, and correctly treating B2B transactions or any sales outside the marketplace scope. For sellers operating across several EU warehouses, this can quickly become a multi-country compliance setup. Without a clear structure, it is easy to lose track of where obligations begin and end, which is why many growing businesses invest early in proper tracking and support.

UK-specific VAT rules (post-Brexit)

The UK operates under its own VAT system, which adds another layer for Amazon FBA sellers working across Europe. For non-UK businesses, VAT registration is usually required as soon as goods are imported into a UK fulfilment centre. The standard domestic threshold of £85,000 generally does not apply in this situation, because the obligation is triggered by the presence of goods in the UK rather than turnover. In simple terms, if your stock is in a UK warehouse, you are expected to be registered and reporting.

Import VAT is an important part of the picture. Many sellers use Postponed VAT Accounting, which allows import VAT to be declared on the VAT return instead of being paid upfront at the border. However, this is not fully automatic. The importer must be VAT registered in the UK and must actively choose to use PVA, often by instructing their customs agent correctly. When set up properly, it helps manage cash flow and avoids tying up funds during import. On top of that, UK marketplace rules add another layer. In certain cases, when goods are already in the UK and sold by an overseas seller through an online marketplace, the marketplace becomes responsible for collecting VAT. These sales are typically still included in turnover reporting but are treated differently from seller-taxable sales. Even so, the seller must continue filing VAT returns, reporting imports, and accounting for any transactions that fall outside those specific marketplace scenarios.

Step-by-Step: Preparing Your VAT Data from Amazon

Step 1 – Map your Amazon FBA footprint

Before you even open a VAT report, you need a clear picture of how your Amazon business actually operates behind the scenes. This means identifying where your stock is physically stored, where your customers are located, and which FBA setup you are using. Many sellers assume their setup is simple because they only sell through one marketplace, but once Amazon starts distributing inventory across its network, things become less predictable. Your products might be stored in multiple countries without you actively deciding it, and each of those locations can create VAT obligations.

Pan-EU FBA makes this even more dynamic. Instead of shipping everything from one country, Amazon spreads your stock across several EU warehouses to speed up delivery. From a logistics perspective, this is great. From a VAT perspective, it creates a presence in each of those countries. These movements are not sales, but they still matter. When your goods move between countries, they are treated as non-transactional transfers, meaning you are effectively transferring goods to yourself across borders. Even though no revenue is generated at that moment, these movements usually need to be tracked and reported. Getting a clear overview of your footprint early makes the rest of the process much easier to manage.

Step 2 – Download Amazon VAT reports

Once your footprint is clear, the next step is collecting the right data from Amazon. The most important report here is the Amazon VAT Transactions Report. This is the core document for VAT purposes because it shows how each transaction is treated, including who is responsible for VAT and what rates apply. It can be accessed through Seller Central in the tax document section, and it should be downloaded regularly so your data stays current and complete.

That said, relying on a single report is not enough if you want to avoid mistakes. You also need inventory and fulfilment reports to understand where your stock is located and how it moves between warehouses. Sales reports for each marketplace help you cross-check totals and confirm that everything lines up. This is where reconciliation becomes important. Your VAT report, sales data, and inventory movements should all tell the same story. If they do not match, it usually means something has been misclassified or missed. Taking the time to compare these sources might feel repetitive, but it is one of the most reliable ways to keep your VAT reporting accurate as your business grows.

Step 3 – Classify each transaction

Raw Amazon data only becomes useful once it is properly structured. This is where you turn reports into something workable, usually by organising everything in a spreadsheet or accounting system. Each transaction needs to be clearly described so you understand what actually happened. This includes identifying the country where the goods were dispatched from, where they were delivered, whether the customer is a business or a private individual, and whether Amazon or you were responsible for collecting VAT. Adding the applicable VAT rate and warehouse location completes the picture and allows you to group transactions logically.

A critical part of this step is separating transactions where Amazon acts as the deemed supplier from those where you remain responsible for VAT. These two categories must be handled differently. If Amazon collects VAT, the transaction is usually recorded differently than a sale where you are the one charging VAT. Mixing them together can lead to incorrect totals and reporting errors. Once your data is structured correctly, patterns begin to appear, and it becomes much easier to assign each transaction to the correct VAT treatment.

Identify transaction types

After classification, the next step is understanding what each transaction actually represents from a VAT perspective. Domestic sales are typically the most straightforward, as they are reported in the country where the stock is stored and delivered. Cross-border B2C sales within the EU may fall under OSS if they qualify as distance sales. However, OSS does not apply to domestic sales from foreign warehouses, stock transfers, imports, or B2B transactions. Import-related sales add another layer, especially when goods enter from outside the EU, where separate VAT rules may apply depending on how the shipment is structured.

B2B transactions require particular attention because they often follow different rules than consumer sales. In many cases, VAT is not charged in the usual way but handled through reverse-charge mechanisms, shifting the responsibility to the buyer. This affects both invoicing and reporting. The key here is consistency. Each type of transaction should be clearly identified and treated the same way every time. When this step is done properly, your VAT returns become much easier to prepare and far less likely to contain errors.

Handle stock movements (“self-supplies”)

One of the more confusing parts of Amazon FBA VAT is dealing with stock movements that are not actual sales. When your goods are transferred from one EU country to another, this is usually treated as a self-supply. In practice, this means you are considered to be making an intra-EU supply in the country of dispatch and an intra-EU acquisition in the country where the goods arrive. Even though there is no customer and no payment involved, both sides of this movement may need to be reported in your VAT records.

To keep things clear and traceable, sellers often create internal transfer documents, sometimes referred to as pro forma invoices, to document these movements. These are not always formal invoices in a strict legal sense, but they help maintain a consistent audit trail. The transfers are usually reported as intra-EU supplies in EC Sales Lists and as acquisitions in the destination country, provided you have a VAT registration there. They may also interact with Intrastat reporting if certain thresholds are exceeded. While this might seem overly detailed for moving your own stock, it is a necessary part of staying compliant. Ignoring these movements can lead to gaps between your inventory records, Amazon data, and VAT filings, which is exactly the kind of mismatch tax authorities tend to notice.

Step-by-Step: Filing VAT Returns (EU + UK)

Step 4.1 – Local VAT returns (stock countries)

Determine filing frequency

Once your VAT registrations are in place, the first thing to understand is how often you are expected to file returns. This is not something you choose freely. Each country assigns a filing frequency based on your status and expected activity. For Amazon FBA sellers, especially those registered as non-residents, monthly filing is quite common at the beginning, even if the sales volume is still relatively modest. Over time, some tax authorities may allow a switch to quarterly reporting, but this depends on local thresholds and your compliance history.

This matters more than it seems at first. Monthly filing means working with tighter timelines, more frequent data preparation, and less flexibility if something goes wrong. If you operate in several countries, you might be dealing with different filing schedules at the same time, which can quickly become difficult to manage without a clear system. Building a routine that matches these obligations early on helps avoid last-minute stress and reduces the risk of missed deadlines or rushed calculations.

Aggregate local sales

Once the timing is clear, the next step is pulling together the right sales data for each VAT registration. This is where your earlier classification work becomes essential. You need to isolate transactions that belong to a specific country, based primarily on where the goods were dispatched from and delivered. In practice, this means focusing on domestic sales linked to stock stored in that country, regardless of which Amazon marketplace the order came through.

Dispatch location is the key driver here. A sale shipped from a German warehouse to a German customer belongs in the German VAT return, even if the order was placed through another marketplace. This is why your inventory data and VAT reports must align. If they do not, it is easy to misallocate sales or overlook them entirely. Accurate aggregation ensures that each VAT return reflects the actual activity tied to that country, which is critical for both compliance and consistency across your filings.

Apply correct VAT rates

After grouping your sales correctly, you need to ensure that the right VAT rates are applied. While Amazon provides VAT-related data, it does not remove your responsibility for correctness. Different countries apply different rates depending on the type of product, and some items may qualify for reduced or zero rates. This means your product classification must match local VAT rules in each country where you operate.

Mistakes here can directly affect your margins and your compliance position. Charging too little VAT can lead to underpayments and penalties, while charging too much can distort pricing and reduce competitiveness. As your product range expands, keeping VAT treatment consistent becomes more challenging, so it is worth establishing a clear internal approach to how rates are assigned and reviewed. This reduces the risk of inconsistencies and makes your reporting more reliable over time.

Report intra-EU movements

In addition to sales, your VAT reporting must also reflect movements of stock between countries. When goods are transferred from one EU country to another, this is treated as an intra-EU supply in the country of dispatch and an intra-EU acquisition in the country of arrival. Even though no sale takes place, both sides of this movement must usually be recorded. This requires you to have VAT registrations in both countries involved in the transfer.

These transfers are reported in EC Sales Lists as intra-EU supplies, using your VAT number in the destination country as the counterparty. This ensures that the dispatch and acquisition sides match across jurisdictions. The same movements must also appear in your VAT returns, creating a consistent record of how goods move within your business. In some cases, they may also trigger Intrastat reporting obligations once country-specific thresholds for arrivals or dispatches are exceeded, and these thresholds vary between EU member states. Keeping these elements aligned is essential to avoid discrepancies between different reporting systems.

Account for input and import VAT

VAT returns are not only about what you owe but also about what you can recover. Input VAT includes tax paid on business expenses, and in many cases, this can be deducted from your output VAT liability. For this to work, the underlying documentation must be correct. Input VAT can only be deducted if it is supported by valid VAT invoices that meet local requirements. If documentation is missing or incomplete, tax authorities may deny the deduction, even if the expense itself is legitimate.

Import VAT is another key element, especially for sellers bringing goods into the EU or the UK. In the UK, many VAT-registered sellers use Postponed VAT Accounting, which allows import VAT to be declared and recovered through the VAT return instead of being paid upfront, provided it is correctly applied in customs declarations. In the EU, recovery of import VAT depends not only on local rules but also on who acts as the importer of record. If the seller is the importer, input VAT is typically recoverable. If another party handles the import, recovery may not be possible. Understanding this distinction is important, as it directly affects your cash flow and your ability to reclaim VAT.

Submit and pay VAT

The final step is submitting your VAT return and settling any tax due. Each country has its own system, deadlines, and technical requirements, and these must be followed carefully. Even small delays can result in penalties, so consistency is key. When preparing your return, it is also important to understand how different types of transactions are treated. When Amazon acts as a deemed supplier, those sales are typically not reported as taxable output VAT in your return, but they may still need to be included in turnover figures depending on local reporting rules.

Managing submissions across multiple countries can quickly become complex, especially as your business grows. This is why many sellers choose to work with VAT agents or accountants who are familiar with local systems and requirements. Whether you handle filings yourself or delegate them, the important thing is that your returns are based on consistent, well-structured data. When everything ties together, from inventory movements to sales classification and final reporting, the process becomes far more manageable and far less prone to costly errors.

Step 4.2 – OSS returns for EU distance sales

Check the 10,000 EUR threshold

Before using OSS, you need to determine whether it actually applies to your business. The key trigger is the 10,000 euro threshold, which covers total cross-border B2C sales of goods and certain services to consumers in other EU countries. This threshold is calculated across the entire EU, not per country, which means even moderate activity spread across multiple markets can push you over it. Once exceeded, you must apply the VAT rate of the customer’s country instead of your home country rate.

Below that threshold, you may continue applying domestic VAT rules, but there is also the option to voluntarily opt into OSS earlier. Some sellers choose this to simplify future scaling or avoid switching systems later. The important part is consistency. Whether you stay below the threshold or opt into OSS voluntarily, your VAT treatment needs to match your actual sales structure and remain stable over time.

Register for OSS

Once you decide to use OSS, registration is done through the tax portal in your home EU country. Your home tax authority becomes the central point for submitting OSS returns and making payments, even though the VAT itself is due to other EU countries. This setup simplifies the administrative side of cross-border sales, but it does not change your underlying obligations in countries where your business has a physical presence.

Even when OSS applies, storing stock in another EU country usually still requires local VAT registration in that country. OSS and local registrations are not alternatives but parallel systems. OSS covers qualifying cross-border B2C distance sales, while domestic sales, stock movements, and other transactions linked to local stock must still be reported through local VAT returns. Understanding this distinction is essential to avoid gaps or overlaps in reporting.

Prepare OSS data

Preparing your OSS return is mainly about filtering the correct transactions and structuring them properly. You need to isolate cross-border B2C sales where goods are shipped from one EU country to consumers in another EU country and qualify as distance sales. Transactions such as domestic sales from foreign warehouses, stock transfers, imports, and B2B activity must be excluded, as they fall outside the scope of OSS.

Once filtered, the data must be grouped by destination country and VAT rate. Each country may have multiple applicable rates depending on the product category, so accuracy at this stage is important. OSS returns only include VAT on sales, meaning output VAT. Input VAT cannot be deducted through OSS and must be reclaimed through local VAT registrations or separate refund procedures. Because of this, your OSS figures need to align with your broader VAT setup, ensuring that sales and recoverable VAT are handled in the correct places.

Submit and pay

OSS returns are submitted quarterly through your home country’s tax portal. Instead of filing separate returns in each destination country for qualifying sales, you submit a single consolidated return and make one payment. Your home tax authority then distributes the VAT to the relevant countries. This reduces administrative effort but does not reduce the importance of accuracy.

One important detail is how corrections are handled. OSS returns cannot be amended in the same way as standard VAT returns. If an error is identified, it is usually corrected in a future OSS return rather than by reopening the original filing. This makes accurate classification and preparation at the start especially important. Small errors can carry forward if not managed properly, so maintaining clean and consistent data is key to avoiding complications later.

Step 4.3 – UK VAT returns for FBA sellers

Report UK domestic sales

For Amazon FBA sellers operating in the UK, domestic VAT reporting is based on where the goods are located at the time of sale. If your products are stored in a UK fulfilment centre and sold to UK customers, those transactions fall within UK VAT reporting. However, not all sales are treated in the same way. In the UK, Amazon is treated as the deemed supplier for certain transactions, particularly where goods are located in the UK and sold by an overseas seller through the marketplace.

This distinction affects how transactions appear in your VAT return. Sales where Amazon acts as the deemed supplier are typically not reported as taxable output VAT, but they may still need to be included in turnover figures, such as Box 6, depending on reporting requirements. Separating these from seller-liable transactions ensures that your return reflects only the VAT you are responsible for, while still maintaining a complete and consistent picture of your business activity.

Handle import VAT

Import VAT plays a central role in UK VAT reporting, especially for sellers bringing goods into the country from outside the UK. Many VAT-registered sellers use Postponed VAT Accounting, which allows import VAT to be declared and recovered through the VAT return instead of being paid upfront. For this to work correctly, the seller must be VAT registered, act as the importer of record, and ensure that PVA is properly applied through customs declarations, often by coordinating with their customs agent.

If Postponed VAT Accounting is not used, import VAT is typically paid at the border and evidenced through C79 certificates. These documents are required to reclaim the VAT through your return. The distinction between these two methods is important because it directly affects cash flow and documentation requirements. Ensuring that your import structure is set up correctly from the start helps avoid issues with VAT recovery and keeps your reporting aligned with customs records.

Include B2B transactions

B2B transactions in the UK require careful handling, even if they represent a smaller portion of your sales. In most cases involving goods, VAT is applied in a standard way, but there are situations where different rules may apply. In certain cases, particularly for services or specific sectors, reverse-charge mechanisms can shift the responsibility for VAT reporting to the buyer instead of the seller.

Even when reverse charge does not apply, B2B transactions must still be clearly identified and treated consistently in your records. This ensures that invoicing, VAT treatment, and reporting all align correctly. Keeping these transactions properly classified is important for maintaining consistency between your UK VAT return and your overall accounting records, especially if your business operates across multiple jurisdictions.

File via MTD

All UK VAT returns must be submitted through the Making Tax Digital system, which requires the use of compatible software or an authorised agent. This means your VAT data must flow digitally from your accounting system into the final submission, with no manual filing allowed. For Amazon FBA sellers, this often involves integrating accounting or VAT tools that can handle the structure of marketplace data.

The move to digital reporting has made the process more standardised, but it also means that errors in your underlying data are more likely to carry through to the final return. There is less room for manual adjustments at the submission stage, so accuracy earlier in the process becomes critical. When your systems are set up correctly, MTD can make filing more efficient, but it depends entirely on the quality and consistency of the data you are working with.

Practical tips and key VAT changes for 2026

Marketplace “deemed supplier” rules

One of the biggest shifts in VAT for e-commerce has been the introduction of marketplace “deemed supplier” rules, and by 2026 these are a core part of how Amazon operates across both the EU and the UK. In the EU, these rules typically apply to certain B2C sales made through marketplaces, especially for imported consignments with a value up to 150 euros and for sales made by non-EU sellers to EU consumers. In the UK, a similar approach applies where goods are located in the UK and sold by overseas sellers through an online marketplace. In these cases, Amazon is treated as responsible for collecting and reporting VAT on the sale to the final customer.

From a VAT perspective, the transaction is split into two parts. First, there is a deemed B2B supply from you to Amazon, even though there may be no physical movement of goods or actual commercial sale between you and the platform. This deemed supply is often treated as a zero-rated intra-EU supply or as outside the scope of VAT, depending on the specific setup and location of the goods. Then Amazon makes the B2C sale to the customer and accounts for VAT on that transaction. In many cases, you are not required to issue a traditional VAT invoice to Amazon for this deemed supply, but you still need to record it correctly in your accounting data. These transactions are typically excluded from output VAT calculations in your return but are often still included in turnover figures and statistical reporting, depending on local rules.

Common misconceptions

A lot of confusion around VAT comes from one persistent myth: that Amazon handles everything. It is easy to see why people think this. The platform calculates VAT on orders, sometimes collects it, and provides tax reports that look quite complete. But this only covers a specific part of the system. The legal responsibility for VAT compliance still sits with you as the seller, and that includes registrations, reporting, and maintaining accurate records across every country where your business has a footprint.

The gaps usually appear when a business starts scaling. Storing stock in multiple countries creates VAT obligations even if Amazon handles part of the sales process. Moving goods between warehouses triggers reporting requirements that have nothing to do with customer orders. Importing products brings its own layer of VAT and customs complexity. These are areas where Amazon does not step in, and where mistakes tend to happen if sellers rely too heavily on the platform. The safest mindset is to treat Amazon as a tool that provides data and logistics support, not as a system that replaces your VAT responsibilities.

Automation and VAT tools (post-2024 landscape)

As Amazon has reduced or restructured parts of its VAT compliance services in recent years, many sellers have moved toward third-party tools and specialised VAT providers. These solutions connect directly to Amazon, pull transaction data, and help organise it into a format suitable for VAT reporting across multiple countries. For businesses that are growing across borders, this shift is less about convenience and more about keeping control over increasingly complex data.

Automation can make a big difference, especially when dealing with multiple VAT registrations, OSS returns, and different filing schedules at the same time. These tools help track deadlines, group transactions correctly, and highlight inconsistencies before they turn into reporting issues. At the same time, they are not a shortcut around compliance. They rely heavily on correct configuration and data mapping. If transactions are misclassified at the source, automation can scale those errors rather than fix them. Looking ahead to 2026, this becomes even more important as additional digital reporting requirements are already arriving — mandatory e-invoicing via KSeF in Poland has been live since February 2026 for large taxpayers and April 2026 for all other VAT-registered businesses, with full enforcement (including financial penalties) from January 2027. These changes push businesses toward more structured and accurate data, making it essential to combine automation with a clear understanding of how VAT rules apply to your setup.

VAT scenarios overview for 2026

How different Amazon FBA setups affect your VAT obligations

By this point, it should be clear that VAT for Amazon FBA is not a single system but a combination of rules that follow how your business actually operates. The most important principle is simple: VAT follows your stock and your transaction flows, not just where your company is registered. As soon as your inventory moves or is stored in another country, your VAT position can change, sometimes without you actively doing anything.

Most sellers move through a few typical stages as they grow. What starts as a simple domestic setup can gradually evolve into a multi-country VAT structure. Understanding these scenarios helps you recognise where you are now and what might come next. It also makes it easier to plan your registrations and reporting instead of reacting when obligations suddenly appear.

Typical VAT scenarios explained

If you are an EU-based seller storing stock only in your home country and your cross-border B2C sales stay below 10,000 euros per year, your VAT setup is relatively simple. In this case, you typically only need a VAT registration in your home country, and all sales are reported through local VAT returns. Below the threshold, you can continue applying domestic VAT rules or voluntarily opt into OSS if you prefer to apply destination-country VAT consistently across EU sales.

Once your cross-border B2C sales exceed 10,000 euros, you are required to apply the VAT rate of the customer’s country. Many sellers choose to register for OSS at this point to simplify reporting. You continue filing domestic VAT returns in your home country, while also submitting quarterly OSS returns for qualifying cross-border B2C sales. Even at this stage, your setup remains relatively manageable as long as your stock is stored in one country.

A very common next step, especially for growing sellers, is storing stock in a single foreign EU country, for example a Polish seller holding inventory only in Germany. In this case, VAT registration is typically required in that foreign country because your stock is physically stored there. Domestic sales in that country must be reported locally, while cross-border B2C sales to other EU countries may still be reported through OSS. This creates a slightly more advanced structure, but still far simpler than a full multi-country setup.

The model becomes significantly more complex when you start using Pan-EU FBA or similar programs where Amazon distributes your stock across multiple EU countries. As soon as your goods are stored in several countries, VAT registration is typically required in each of them. You then need to file local VAT returns in every storage country, while OSS can still be used for qualifying cross-border B2C sales between countries. Even when using OSS, storing stock in another country generally still requires a local VAT registration there. This creates a hybrid system where local reporting and OSS operate in parallel.

For non-EU sellers using Amazon FBA in Europe, VAT obligations usually begin immediately. Importing goods into the EU and storing them in warehouses typically requires VAT registration from the start, without relying on thresholds. On top of that, in many EU countries non-EU sellers are required to appoint a fiscal representative, which adds another layer of compliance and cost. Even if Amazon collects VAT on certain B2C transactions under marketplace rules, the seller still needs to manage local VAT returns, stock movements, and import-related reporting across each country where goods are stored.

The UK follows a similar logic but operates under its own VAT system. If you are a non-UK seller storing goods in a UK warehouse, VAT registration is required from the first taxable transaction. The UK domestic VAT threshold does not apply in this situation. You are expected to report domestic sales, handle import VAT, and file VAT returns through the UK system. In the UK, marketplace rules apply particularly where goods are located in the UK and sold by overseas sellers through platforms like Amazon, meaning Amazon may collect VAT on certain transactions, but this does not remove your broader reporting obligations.

How to interpret these scenarios in practice

These scenarios are not fixed categories that you choose once and stay in permanently. Most sellers move between them as their business grows, often without noticing exactly when their VAT obligations change. A business might start with a simple domestic setup, then exceed the OSS threshold, later store stock in another country, and eventually expand into a full Pan-EU structure. Each step adds a new layer of complexity, even if your day-to-day operations feel similar.

It is also important to remember that marketplace deemed supplier rules can apply within many of these scenarios. In certain cases, Amazon collects VAT on B2C sales, but this only covers specific transaction types. It does not replace your need to register for VAT, report stock movements, or file returns for other activities. The key takeaway is that VAT is closely tied to how your business operates in practice. By understanding which scenario you are currently in, you can stay ahead of your obligations and build a system that scales with your growth instead of becoming a problem later.

Conclusion: From chaos to control

Making sense of your VAT setup as you grow

If there is one thing to take away from all of this, it is that VAT in Amazon FBA is not random, even if it feels that way at first. It follows a clear logic, but that logic is tied to how your business actually operates. Where your stock is stored, how it moves between countries, and who you sell to all shape your VAT obligations. Once you understand that VAT follows your inventory and your transaction flows, the system starts to feel less chaotic and more predictable.

At the same time, accuracy becomes everything. Amazon gives you a huge amount of data, but that data only becomes useful when it is properly structured and understood. Small mistakes in classification can quickly turn into larger reporting issues, especially when you are dealing with multiple countries, different VAT treatments, and parallel systems like local returns and OSS. The more consistent your data is from the start, the easier it becomes to manage your VAT as your business grows.

VAT as part of your business infrastructure

Another important shift in mindset is seeing VAT not as a one-off task, but as part of your operational setup. Once you move beyond a single-country business, compliance becomes layered. You might be dealing with local VAT returns in several countries, OSS filings for cross-border sales, and separate rules for the UK, all at the same time. Add to that stock movements, imports, and marketplace rules, and it becomes clear that VAT is woven into your daily operations, not something you handle once a quarter and forget.

The final takeaway is simple but important. VAT is not optional, and it is not something you can fully outsource to Amazon or automate away without understanding it. It is part of the infrastructure of your business, just like logistics, pricing, or product sourcing. When you treat it that way, build systems around it, and stay consistent with your data, it stops being a source of stress and becomes something you can manage with confidence as you scale.